You can score overrun with debt, however, debt consolidating even offers a simple solution. Bankrate’s debt consolidation reduction calculator was created to make it easier to know if debt consolidating is the proper circulate for you. Merely fill out your an excellent loan wide variety, bank card stability or any other debts. Next see what the brand new monthly payment was with an excellent consolidated loan. Is actually modifying this new terms, mortgage types or price unless you select a debt settlement bundle that suits your aims and you can funds.

Debt consolidation involves merging multiple expenses to your you to the brand new financing. The goal is to improve repayments, down focus, and you can pay back financial obligation quicker. Bankrate’s debt consolidation calculator was created to help you know if debt consolidation reduction is the best move to you personally.

Fill in your own a great financing number, mastercard stability and other debts to see what your month-to-month commission you are going to appear to be. Is modifying the fresh new terminology, loan sizes otherwise price if you do not come across a debt negotiation bundle that suits your aims and you can budget.

5 a method to combine loans

When you work with the quantity, choose an easy way to combine your debt. You can find pros and cons to each choice and you can, as ever, you should look around to have financial products to make sure you are acquiring the most useful speed and you can conditions.

Keep in mind that debt consolidation reduction is not suitable people. You will want to merely consolidate your debt for individuals who be eligible for a beneficial lower rate of interest than you are currently spending. It is extremely important to remember that only some types of personal debt might be consolidated.

step one. Personal loans

A personal loan was an unsecured loan one, in lieu of credit cards, possess equivalent monthly obligations. Mortgage numbers are very different having credit history and you can record, but fundamentally finest aside within $100,000. Whenever you are banking institutions and you will borrowing from the bank unions offer signature loans, subprime loan providers are extremely active inside market, therefore store very carefully and you can contrast prices, words and you may charges anywhere between around three or more loan providers.

Since an unsecured loan try unsecured, there are no possessions at risk, it is therefore recommended to possess a debt consolidation financing. Although not, know that a large financing that have a reduced Apr needs a good credit score. Here are some ideal personal loans getting debt consolidation reduction and you can evaluate lenders to find the best personal loan price for your requirements.

dos. Family equity finance otherwise personal lines of credit

Once the a resident, you are able to this new equity of your property to help you combine their obligations. Since house equity money and you can lines of credit (HELOCs) have all the way down interest levels, they may cost a lower amount than simply a personal bank loan otherwise equilibrium import mastercard. not, bringing extended to repay the loan you will mean expenses much more inside the focus.

Home security financing can be a dangerous style of loans integration. If you cannot pay off the mortgage, you could dump your home to foreclosures.

step 3. Charge card transfers of balance

Moving the debt to a single mastercard, labeled as a charge card harmony import, could help you save money on appeal. New card will demand a limit high enough to match your balance and you will an annual percentage rate (APR) reasonable adequate to build combination practical.

Providing an unsecured card ensures you might not risk any property. Before applying, inquire about balance import limits and fees. As well as, you generally wouldn’t find out the Annual percentage rate otherwise credit limit until shortly after and you can unless you are acknowledged.

Using one bank card because the data source for all your card financial obligation was fighting fire with flames, very be cautious should this be the policy for debt consolidation reduction. After you’ve moved expenses to 1 card, manage purchasing you to definitely cards off as fast as possible – and avoid wracking upwards additional loans on your other notes.

cuatro. Deals or later years profile

- Family savings: You are able to their discounts to pay off all the otherwise a good part of the debt. However it may not be the top. For many who acquire of deals, you might be remaining in place of an emergency finance to cover unforeseen expenses later on.

- 401(k): Of several 401(k) agreements allows you to borrow against pension discounts during the a beneficial apparently low-value interest. But when you quit your work or get fired, the entire 401(k) financing becomes due quickly. Even though you are safe on the business, discover a 10 % penalty extra if you can’t pay and you are clearly less than decades 59.5.

- Roth Private Senior years Account: There’s no punishment having borrowing from the bank what you transferred on your own Roth IRA, however you will desire to be sure merging obligations outweighs the fresh new lost dominating and you will substance attention.

5. Financial obligation management agreements

If you prefer debt consolidation reduction alternatives that don’t want taking out fully financing, trying to get a unique credit or tapping into offers or senior years membership, a debt government plan will probably be worth considering. That have a debt management plan, you can easily work at good nonprofit borrowing from the bank counseling institution in order to discuss with loan providers and you will draft a propose to pay back the money you owe.

Your close most of the credit visit here card profile and work out that payment per month for the department, and that pays this new loan providers. You still receive the battery charging statements out of your financial institutions, so it is an easy task to song how fast your debt is paid down.

Certain enterprises will get work for lower if any cost while struggling with your bank account. Stick to nonprofit firms connected to the fresh new Federal Foundation to possess Borrowing Guidance or the Economic Guidance Relationship of The usa, and make certain your debt counselor are formal through the Council to the Certification.

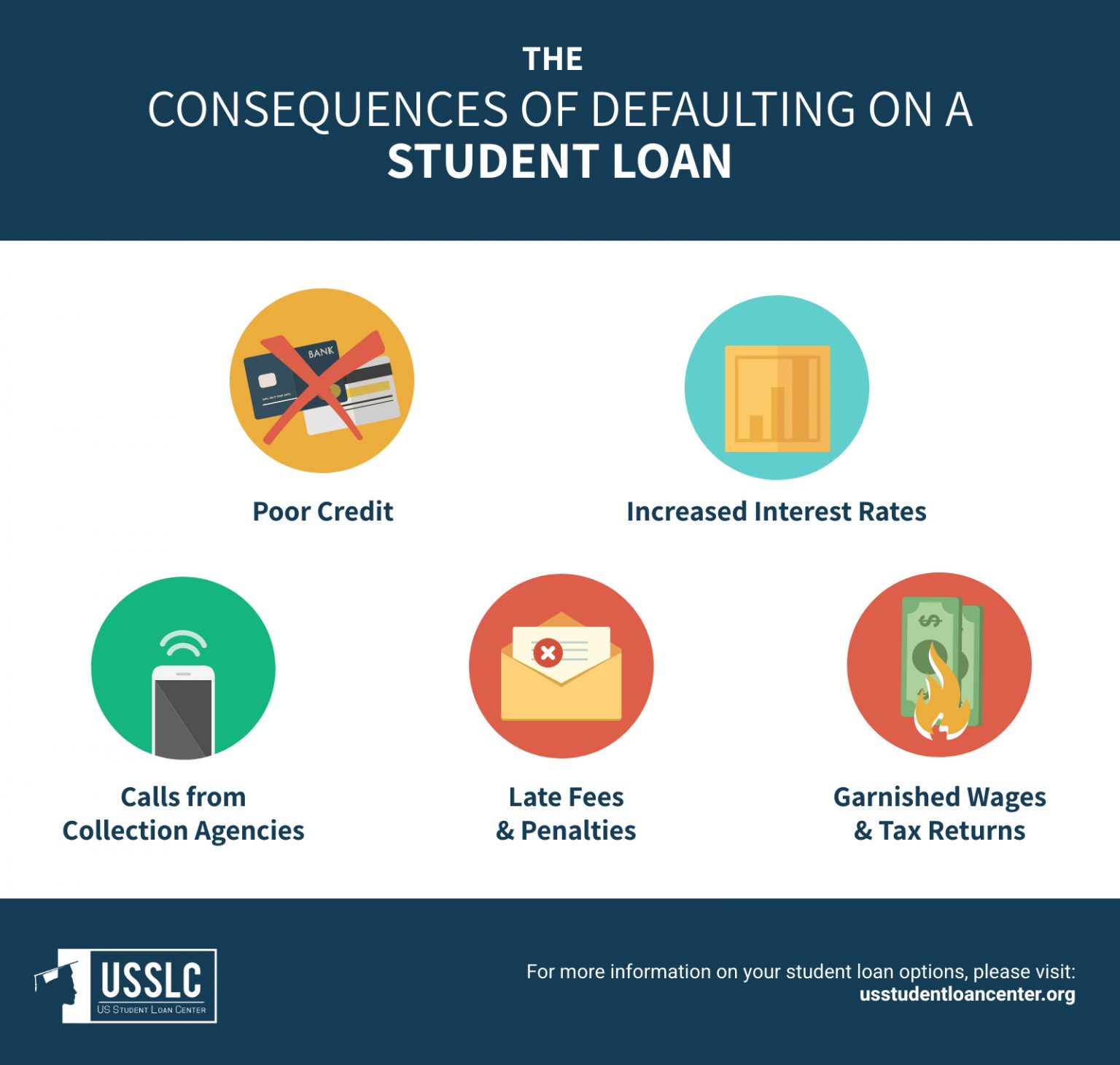

Normally debt consolidating harm my credit score?

Debt consolidation fund normally damage your credit score, however the perception is usually brief. Applying for the borrowed funds concerns a painful credit score assessment, that will get rid of the rating by several circumstances, predicated on FICO.